Natural Resource Fund (NRF) in a Developing Society: Insights from the State Oil Fund of Azerbaijan (SOFAZ)

University of Glasgow, United Kingdom

Abstract. This paper examines the State Oil Fund of Azerbaijan (SOFAZ), analysing its evolution and performance as a Natural Resource Fund (NRF) in an institutionally developing society. The analysis highlights SOFAZ’s initial challenges in curbing overspending of oil revenues, attributed to weak oversight and socio-economic pressures. The 2015 oil price decline prompted the government to shift its strategy by focusing on reducing budget transfers from SOFAZ, a goal that was achieved to a certain degree. The paper examines the role of transparency and the public availability of financial information about the fund as political incentives in this shift. However, it cautions that such transparency should not be equated with full public accountability, especially since significant economic challenges remain. While SOFAZ’s transparency measures have contributed to its relative stability, the fund’s long-term sustainability depends on continued efforts to reduce budget transfers from the fund. As Azerbaijan navigates its transition to a post-oil economy, the future of SOFAZ’s accumulated assets hinges on maintaining these policy shifts.

Keywords: Natural Resource Fund (NRF), Azerbaijan, resource revenues management, economic policy, transparency.

Index

3.3 Socio-economic projects and investment policy

4.1 Evolution: Before and After 2015

4.2 Role of transparency: incentives and limitations

It is well recognized that nations relying heavily on revenue from exporting non-renewable natural resources – particularly oil and gas – are forced to confront certain economic challenges. These challenges primarily arise due to the volatility, substantial size, and finite nature of the resource revenues. The situation is often exacerbated by governments’ tendency to rapidly spend these revenues without considering the ability of their economies to absorb them effectively. Establishing a Natural Resource Fund (NRF)1 is one way to respond to these challenges. NRFs are institutions designed to collect surplus natural resource revenues, preventing them from flowing directly into the government budget.

Numerous research-rich countries have adopted this strategy with differing levels of success. For example, the Government Pension Fund of Norway (GPFN), frequently referred to as the Norwegian Oil Fund, is widely regarded as one of the most successful examples of an NRF. As the largest NRF globally in terms of assets under management (AUM), it plays an important role in Norway’s fiscal system (Moses 2021). In contrast, Venezuela has faced significant challenges in managing its NRFs, largely due to political instability and a lack of adequate oversight mechanisms, which allowed the governments to deplete the funds (Di Bonaventura Altuve 2024).

The success of any NRF depends significantly on its fiscal policies, such as the rules governing deposits and withdrawals. However, it is also crucial that politicians adhere to these rules. This is particularly important in developing societies, where institutional robustness, oversight, and accountability may not yet meet optimal standards. In such contexts, it could become difficult to prevent the government from mismanaging the fund when it has the incentive to do so. As a result, government may change or ignore NRF regulations, leading to overspending of resource revenues, which undermines the fund’s primary objective of achieving long-term economic stability. In such cases, transparency in terms of the availability of information regarding the fund finances is often seen as one of the critical factors, since “publicizing financial reports, could contribute in countering unauthorized use of funds” (Sanchez and Lamchek 2023, 4). However, while transparency can improve accountability and strengthen government capacity, it is also possible that it may not be sufficient on its own to guarantee the sustainability of NRFs in weak governance settings.

The State Oil Fund of Azerbaijan (SOFAZ) provides a compelling case study of how an NRF operates within the framework of a developing, post-Soviet, society. The fund became operational just before significant oil revenues began entering the Azerbaijani economy in the early 2000s. It was designated that the revenues accumulated in SOFAZ would be saved for future generations and used to ensure macroeconomic stability. The fund’s success in achieving these objectives, however, has been mixed. While SOFAZ has been crucial in stabilizing the economy by providing annual transfers to the state budget, this has also contributed to a growing dependence on the use of oil revenues for public spending, rather than leading to broader economic diversification. Ideally, a well-functioning NRF should help mitigate such dependence.

On the other hand, the fund has also managed to accumulate relatively substantial revenues over the years, with its assets as of 31 March 2025, surpassing sixty-two billion US dollars (SOFAZ Recent figures 2025). This is quite a significant amount for a small country like Azerbaijan, evidenced by the fact that at the end of 2023, SOFAZ’s assets represented 77.5 percent of Azerbaijani GDP, demonstrating the fund’s impressive size relative to the national economy (SOFAZ Annual Report 2023, 44). Moreover, in general, SOFAZ has been recognized for its transparency (Frynas 2017, 137), especially in terms of the public availability of information regarding its financial flows and operations, which are subject to external audits (SOFAZ Annual Report 2023, 63). It is arguably the most transparent institution in the country in this aspect, and this has been achieved despite the fund operating in a political environment with limited oversight.

Notably, in some other cases of NRFs established in institutionally developing societies (e.g. Angola), even the adoption of transparency guidelines ultimately failed to help preserve oil revenues in a sustainable manner due to weak oversight mechanisms and political factors. In contrast to such NRFs in comparable developing societies, SOFAZ has managed to maintain consistent growth of its assets so far. This paper, therefore, seeks to address the following question: What role has transparency played in the long-term sustainability of SOFAZ assets? By analysing SOFAZ’s performance since its establishment, the paper also attempts to offer insights into the extent to which transparency can help sustain NRF assets in a context where formal oversight mechanisms remain weak.

To answer this question paper analyses the performance of the fund before and after 2015 fall of the oil prices, while also evaluating its outlook in light of the expected decline in Azerbaijan’s oil reserves and revenues in the near future. To examine these issues, a qualitative analysis is conducted using official documents such as SOFAZ’s annual reports and government decrees. This is complemented by a review of secondary sources, including academic research and media sources, to provide context and assess SOFAZ’s overall performance. The paper is structured as follows: Section 2 provides an overview of NRFs, including their functions and related literature. Section 3 examines the operation and performance of SOFAZ since its inception. Section 4 delves into role of transparency. Section 5 provides an analysis of the future prospects of the fund and concludes.

NRFs have existed since the 1950s.2 Over the years, many resource-rich countries have established such funds with the hope of better managing their large and highly volatile resource revenues. The NRFs may differ from each other in structure. Some are independent legal entities (e.g. Qatar), while others are managed within central banks (e.g. Kazakhstan). Despite these differences in structure, all NRFs are usually established to address the two major problems faced by the countries where resource revenues constitute bulk of the income: the volatility of these revenues and their finite nature. The NRFs tackle these issues by performing their two main functions: stabilization and saving. There is also an additional supplementary function called sterilization, which is closely linked to both of these main functions.

The volatility of resource revenues primarily stems from the fact that market prices for resources fluctuate and often follow a boom-and-bust cycle. If a government does not implement measures to manage this volatility, public spending may also become volatile. NRFs can help mitigate this volatility by performing stabilization. Stabilization occurs when the fund accumulates excess resource revenues during periods of higher-than-average prices and then uses them to support (stabilize) budget expenditures when prices are lower than average or during recession period. This results in a countercyclical spending pattern,3 which is considered fiscally more viable for resource-exporting countries (Snudden 2016).

Alongside being volatile, the revenues derived from non-renewable natural resources are also finite and will eventually be exhausted. This raises concerns about intergenerational equity – the right of future generations to also benefit from the revenues. The savings function of an NRF addresses this question by saving the excess revenues for the benefit of future generations, who are expected to live in times when natural resources will be depleted. These saved revenues can also be invested, preferably abroad, so that the fund’s assets would continue to grow through the returns on this investment, even after the non-renewable resources have been exhausted (Bauer 2014, 14).

The third function NRFs perform (usually integrated with the first two) is sterilization. This process involves managing the appreciation of the national currency’s real exchange rate, which can occur when large amounts of foreign currency flood the economy due to large inflows of resource revenues. This appreciation can harm the competitiveness of the non-resource tradable sector, a phenomenon known as “Dutch disease” (Corden and Neary 1982, Corden 1984). The appreciation of the real exchange rate creates inflationary pressures by boosting domestic spending during a resource price boom. This makes non-resource exports (e.g. manufacturing) more expensive and less competitive abroad, while imports become cheaper. In the 1970s, following the discovery of large gas fields in the North Sea, this led to the decline of the Dutch manufacturing sector (Roy et al. 2013). Since then, many resource-exporting nations, particularly in developing countries, have experienced similar effects (Mien and Goujon 2022). Dutch disease can also contribute to overreliance on the resource sector and make the economy more vulnerable to resource price volatility. By removing (sterilizing) the foreign currency from the economy and using an NRF to invest in assets abroad, the adverse effects of Dutch disease can be mitigated.

While countries may opt to establish two separate funds to address stabilization and savings separately, most exporters usually prefer to establish one single fund that addresses both issues simultaneously, since a unified fund can reduce financing costs and optimize investment returns (Frynas 2017, 127). However, the specific rules governing stabilization and savings vary across NRFs.

The literature on Natural Resource Funds (NRFs) is closely tied to the broader discourse on how natural resource wealth affects the economic outcomes of exporting countries. Many studies highlight the negative effects of natural resource abundance – the so-called “resource curse” – which has been linked to poor economic growth, especially in developing countries (Auty 1993, Sachs and Warner 1995, Karl 1997, Ross 2012, Venables 2016). Similarly, the “rentier state” theory, which looks at the political effects of resource abundance, argues that resource revenues (rents) allow governments to gain an alternative income source to taxation of the population. Such governments become fiscally independent and autonomous from accountability to their population (Mahdavy 1970, Beblawi 1987). Moreover, mismanagement of the resource revenues has been linked to a number of other governance-related issues, including rent-seeking, increasing levels of corruption, patronage politics, deterioration of governance institutions (Karl 1997, Mehlum et al. 2006, Ross 2012, Prichard et al. 2018).

Properly managed NRFs can act as a check on such mismanagement by isolating the resource revenues from the general budget income, thereby supporting the fiscal sustainability in resource-exporting countries. In light with this, research on NRFs often focuses on the analysis of the elements crucial for optimal design within the context of economic management – such as the most effective deposit and withdrawal rules, the degree of alignment of the fund with the country’s broader fiscal policy, or government’s ability to maintain budget surpluses (Davis et al. 2003, Segura 2006, van der Ploeg and Venables 2011, Deléchat et al. 2017).

These fiscal issues aim to enhance NRF sustainability and are undeniably important. However, their effectiveness can be undermined by political dynamics and weak institutional oversight. In practice, NRFs are not only governed by economic policies; political decisions also play a significant role. Governments often face incentives to spend rather than save resource revenues, particularly in weaker institutional settings where even well-designed fiscal rules can be easily bypassed due to weak oversight, which also allow political leaders to take a direct role in the fund management, thus reducing its general effectiveness (Humphreys and Sandbu 2007, Collier et al. 2010, Bernstein et al. 2013, Bauer 2014). As a result, either a very small portion of the revenues is saved, or the saved revenues are eventually depleted, as seen in Venezuela’s FIEM and FONDEN funds (Di Bonaventura Altuve 2024, 292).

The tendency to spend rather than save in developing societies is influenced by more objective, factors as well. First, saving must occur during periods of high resource prices when there is surplus revenue, and the population is least likely to accept low public spending. In developing countries, such as Ghana, directing revenues to an NRF polarized various segments of society, who questioned the choice to save for future generations while facing economic and developmental challenges today (Ackah and Gyeyir 2021, 134). Developing countries are also usually capital-scarce and require investment in building up such capital. Therefore, using resource revenues for such spending (at least in the early period of the revenue influx) is expected and hard to avoid (Collier et al. 2010). In Timor-Leste, for example, the withdrawals from the NRF exceeded the fiscal rules, partly because the rules were too restrictive for a country that required large public spending (Bauer 2014, 21). All these factors can further encourage governments to bypass NRF regulations

Therefore, it is important, when designing economic policies for the management of NRFs (e.g. fiscal rules), to “create political incentives (or at least mitigate political disincentives) for abiding by that policy” (Humphreys and Sandbu, 2007, 226). The role of transparency is particularly emphasized as a crucial element in this discussion (Humphreys and Sandbu 2007, Bauer 2014, Okpanachi and Tremblay 2021, Sanchez and Lamchek 2023). At a minimum, such transparency means that an NRF should, in a timely and constant manner, publicly provide full information about its financial flows. Humphreys and Sandbu (2007, 214) see this as the informational role of NRFs and argue that “when information is scarce and asymmetric, efficient outcomes are more difficult to sustain. An NRF could alleviate this problem by facilitating the flow of information within the government system and between it and the population or the international public”. They also suggest that this transparency could enhance the government’s technical capabilities and potentially encourage greater transparency in other areas. Not surprisingly, the International Forum of Sovereign Wealth Funds (IFSWF)4 and the Truman Scoreboard Index5 view transparency as a key factor for NRF effectiveness and assess it based on factors like public reporting, external audits, and governance structures.

However, it is debatable whether transparency alone is enough to effectively prevent NRF mismanagement, particularly in institutionally weak and developing contexts. Even when a fund is designed with transparency mechanisms and scores highly on international transparency ratings, overall bad governance in the country can override these efforts and lead to fund mismanagement, as seen in examples like Angola (Frynas 2017, Markowitz 2020, Ambe-Uva and Martin 2021). In most cases, such NRFs become unsustainable and save very little or are depleted within the first signs of economic troubles.

Azerbaijani SOFAZ is an intriguing case study for examining the effectiveness of NRF in a developing society. The fund combines stabilization and savings functions and, as an extra-budgetary, separate legal institution has a degree of autonomy from other national financial institutions. SOFAZ is recognized (Luong and Weinthal 2010, Guliyev 2013, Frynas 2017) for its transparency, particularly in terms of publicly (and timely) releasing information about its operations. It is also very highly ranked (scoring 92 out of 100) by the Truman Scoreboard Index (Maire et al. 2021). However, the fund also functions in a society where common oversight mechanisms and wider societal governance are weak (Franke et al. 2009, Guliyev 2020, Umudov 2021).6 This raises an important question for SOFAZ: to what extent has transparency played a meaningful role in fund’s long-term sustainability, or does it merely serve as a symbolic measure? The next two sections of the paper attempt to analyse this dynamic by assessing SOFAZ’s performance since its inception and focusing on the role of transparency.

SOFAZ was established in 1999 and became operational in 2001, making Azerbaijan the first of the post-Soviet oil and gas rich countries to create an NRF. The fund has three main goals: (1) ensuring macroeconomic stability; (2) achieving intergenerational equity; (3) financing major projects to support socio-economic development (SOFAZ Mission and Objectives 2025). While these objectives are typical for most NRFs, it has been argued that in the case of SOFAZ they need to be more detailed, particularly in terms of the connection to the operational rules (Bauer 2014, 20).

The primary revenue source of the fund is the income generated by the sale of Azerbaijan’s oil and gas shares by foreign oil companies (FOCs). Other sources of income include bonus payments, acreage fees, transportation fees paid to Azerbaijan for the transit of oil and gas through its territory, and revenues from the investment returns (SOFAZ Annual Report 2023). It should be noted that revenue from the state oil company SOCAR’s own onshore oil fields is not directed to the fund. FOCs also pay their taxes directly to the state budget. Nevertheless, the greatest portion of the oil wealth is still managed by SOFAZ.

SOFAZ is an extra-budgetary, legally independent institution. However, in terms of oversight, the fund is much more accountable to the executive branch. For example, the president appoints the fund CEO, their deputy and the members of the fund’s seven-member supervisory board. Theoretically, the board has several powers, including, the review and evaluation of the fund’s draft annual budget, financial statements, annual reports, and other related documents (SOFAZ Annual Report 2023). The current board consists of the prime minister, the chair of the central bank, the deputy chair of the parliament, two ministers, and two assistants to the president (SOFAZ Annual Report 2023). This means that six out of the seven members are affiliated with the government, with only one representative from the legislature and no members from civil society. Such structure grants considerable discretion to the executive in managing SOFAZ assets.

The fund’s annual budget is also approved and signed by the president without requiring legislative consent. However, majority of SOFAZ expenditures, particularly budget transfers, are incorporated into the annual national budget, which is debated and approved by parliament (SOFAZ Annual Report 2023). Thus, parliament does exercise certain oversight over the fund withdrawals through the consolidated government budget, although this oversight remains indirect. However, it should be noted that in general, the parliament in Azerbaijan is not regarded as strong, with the members of the ruling party and its affiliates holding the majority of seats (Guliyev 2020, Umudov 2021).

Annual transfers to the state budget are the primary method through which the fund can claim to have achieved its first objective – ensuring macroeconomic stability. These transfers also constitute the bulk of SOFAZ’s annual expenditure. Overall, the fund has transferred $125.1 billion to the state budget between 2003 and 2023 (SOFAZ Annual Report 2023). Before 2019, there were no specific guidelines for determining the annual transfer amounts. The only existing document in this regard was the “Long-Term Strategy on the Management of Oil and Gas Revenues”7 for the period 2005-2025, adopted in 2004 and repealed in 2019 (following the adoption of a new budget rule).

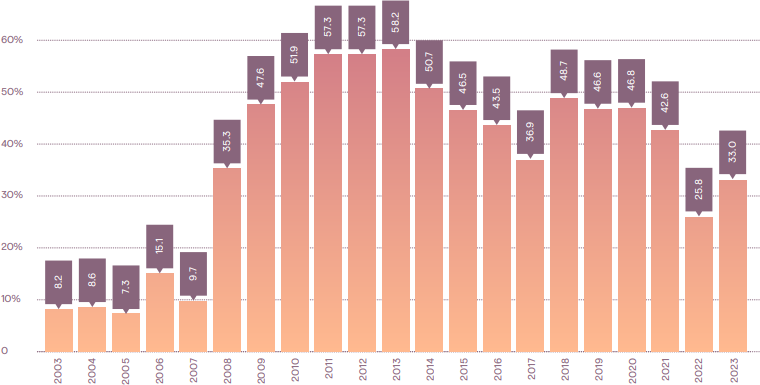

Although this strategy envisioned using the non-oil deficit limit8 to guide medium-term oil revenue spending, this approach was rarely consistently applied. Therefore, evaluating the impact of budget transfers – particularly in the early years of the fund – can be challenging. Figure 1 shows the share of SOFAZ transfers in the state budget revenues from 2003 to 2023, while Figure 2 presents the average annual oil prices during the same period.

As can be seen, the significant rise in the share of transfers within the budget revenues started in 2008, coinciding with the global financial crisis and the decline of oil prices after the mid-2000s oil boom. This period effectively was the first test of SOFAZ’s stabilization function, and it could be argued that it passed this test successfully by shielding the state budget from oil price fluctuations. However, even after oil prices stabilized and rebounded by the end of 2010, the transfers did not decrease, and spending did not become countercyclical. Instead, the share of transfers within budget revenues reached 58.2 percent by 2013, which meant that the government spent around 90 percent ($15.7 billion) of the annual revenues received by the fund (SOFAZ Annual Report 2023). Additionally, these years marked peak Azerbaijani oil production, with the fund receiving more than $16 billion in each of these four years – something that has not been repeated. In summary, during this period, the government was both receiving substantial oil revenues and spending them rapidly, indicating that SOFAZ was not effectively stabilizing or curbing government overspending of oil revenues. It is possible that the large transfers during this period may have also been motivated by political considerations to maintain public spending and political stability.

The change in this strategy began with the sharp drop in oil prices in 2015. This led the government, for the first time, to withdraw more from SOFAZ for a budget transfer than the fund’s total revenue for that year (SOFAZ Annual Report 2023, 2). As a result, the fund’s assets were reduced compared to 2014. This might have been a concerning indicator that the government was beginning to deplete SOFAZ’s assets. Not surprisingly, there were views (Altstadt 2017, 221) that questioned the ability of the fund to survive in such environment.

However, instead, the government enacted several measures, including the devaluation of the national currency, the manat and some optimization of public spending. This led to the gradual reduction of budget transfers, as illustrated in Figure 1. Additionally, there was some economic liberalization aimed at boosting non-oil sectors, and the country introduced several “strategic road maps” to further develop these sectors (President.az 2016). While the effectiveness of these measures can be debated, by 2017, the proportion of budget transfers fell below 40 percent for the first time in nearly a decade. Despite a subsequent rise in transfers after 2017, the 2015-16 period clearly influenced the government, which, in 2019, finally adopted a budget rule that linked transfer calculations to specific guidelines. Although the introduction of the rule was a positive step, its overall complexity was seen as an obstacle to successful implementation (Aghayev 2021).

Once, the Covid-19 pandemic struck, the use of the budget rule was suspended. After the pandemic, government adopted a revised, simpler budget rule at the end of 2021. The new revised rule restricts how large the non-oil budget deficit can be compared to the non-oil GDP. To put it simply: if the limit is 20 percent and the non-oil GDP is expected to be $40 billion, then the maximum allowable non-oil deficit would be $8 billion.9 Since the non-oil deficit is funded by oil revenues (mainly through budget transfers) the limit in theory forces government to stay disciplined and not to overspend from SOFAZ.

Following the adoption of the rule, as Figure 1 illustrates, budget transfers dropped to about a third of budget revenues in 2022 and 2023. However, this is likely due to the rise in energy prices caused by the Russian invasion of Ukraine, which led to higher-than-expected revenues. Thus, the full impact of the new rule remains to be seen. Nonetheless, the decision not to dramatically increase the budget transfers (from 2022 to 2023) during this new boom period can be viewed as a tentative positive development.

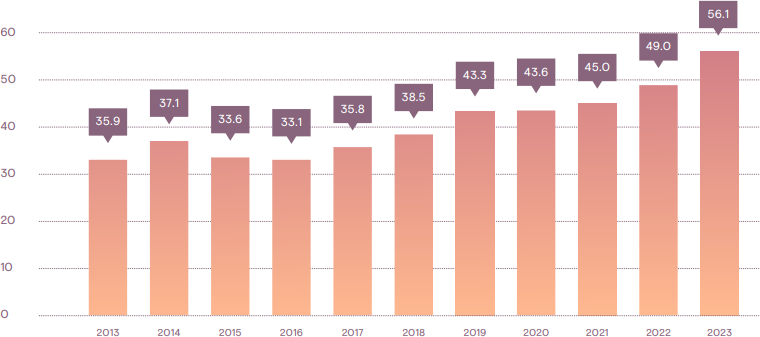

There never were definitive rules specifying how much of the oil revenues should be saved by SOFAZ. The only ambiguous guideline in the “Long-Term Strategy” discussed earlier indicated that, when oil and gas revenues peaked, at least 25 percent should be saved. The document did not clarify whether this 25 percent should be saved annually or define the peak period. The early 2010s seem to be the most likely option, and during that time, the rule (if intended as an annual savings rate) appears to have been ignored. Nonetheless, as shown in Figure 3, the growth of SOFAZ’s assets (which includes both saved oil revenues and investment returns) from 2013 to 2023 was notably positive.

As seen, excluding 2015 and 2016, SOFAZ has always had growth in its assets. Although the positive trend in savings was not always guided by a consistent strategy – as evidenced by the absence of rules governing the savings rate – it still indicates that the government acknowledges the importance of accumulating these assets. By the beginning of 2025, the fund’s assets had reached sixty billion US dollars, which is substantial for a country the size of Azerbaijan (SOFAZ Recent figures 2025).

SOFAZ’s ability to accumulate reserves, even in the periods of economic downturns, distinguishes it from NRFs in other similar resource-rich developing countries. For example, the assets of the National Fund of the Republic of Kazakhstan (NFRK), which have generally fluctuated since 2015, equalled around $59.1 billion by the end of April 2024 (Time.kz 2024). Given Azerbaijan’s much smaller oil reserves and the similar establishment timing of the funds, SOFAZ’s closeness to NRFK in terms of the size of its assets is impressive.

While the newly adopted budget rule does not explicitly address the savings rate, it may indirectly influence asset growth by potentially reducing budget transfers. The decree signed in October 2023 (E-qanun.az 2023), aims to decrease the limit on the ratio of the non-oil base deficit to the non-oil GDP, lowering it from 24 percent in 2024 to 17.5 percent in the medium term. If implemented, this should lead to a reduction in budget transfers and a further increase in the share of saved revenues.

3.3 Socio-economic projects and investment policy

The revenues transferred from the fund to the state budget through the annual transfers were already used to finance the socio-economic projects via traditional public spending channels. However, from 2001 to 2023, the fund also spent an additional $11.8 billion to directly finance certain key projects (SOFAZ Annual Report 2023). In these cases, SOFAZ provided funding to state entities responsible for implementing the projects directly, bypassing the centralized state budget.

One of the principal areas where SOFAZ funds were used was the improvement of the living conditions of refugees and IDPs from the war with Armenia. Other directly financed projects include improvements to the water supply system of Baku, the construction of the Baku-Tbilisi-Kars railway, energy-related projects (e.g. the Southern Gas Corridor), education-related projects and others (SOFAZ Recent figures 2025). Many of these are already completed. Generally, such direct investments from an NRF are undesirable (Humphreys and Sandbu 2007) and SOFAZ has been criticized for engaging in it (Bauer 2014, 5). It is more efficient and transparent to have one single expenditure source, namely the national budget. Therefore, the gradual winding down of such spending recent years is a positive development.

Finally, the investment policy of SOFAZ also deserves attention. The fund’s investment portfolio is managed based on the annual guidelines approved by the president (SOFAZ Annual Report 2023). The fund invests in fixed-income instruments, equities, gold, and real estate. Its investment policy has always been defined by conservatism. Low-risk, low-yield fixed income makes up the majority of the fund’s portfolio. This is not surprising. While equities offer the potential for higher returns, they also come with greater risk, which is unacceptable given the critical role of the fund’s assets in budgetary transfers. In this conservatism, SOFAZ is not so different from other relatively smaller NRFs. Usually, only the largest NRFs (e.g. Norway) are in position to pursue riskier investments. Overall, since its inception, SOFAZ has generated $11.5 billion in investment revenue, which accounts for 5.8 percent of the fund’s total revenues until 2023 (SOFAZ Annual Report 2023).

4.1 Evolution: Before and After 2015

The previous section evaluated the stabilization and saving functions of SOFAZ. However, as this paper has argued, simply analysing economic policies is not enough to evaluate an NRF. The institutional and political context is also important. In this respect, it may be helpful to divide the operation of SOFAZ into two phases: before and after 2015.

Before 2015, the fund exhibited many of the limitations typical of an NRF in a developing society. During this period, the government tended to spend heavily and was inconsistent in applying what were, in effect, very ambiguous fiscal rules. Insufficient oversight mechanisms, coupled with strong, centralized executive control over the fund and a weak legislature, were clearly important contributory factors. It is also evident that spending acted as a tool for the government’s political consolidation, by, for example, financing expenditures ahead of elections (Kendall-Taylor 2012, Guliyev 2013).

However, understanding the broader context behind this spending is also important. Azerbaijan faced a severe economic decline in the early years of its independence as the country’s GDP fell from $8.8 billion in 1990 to $1.9 billion in 1994 (Data.worldbank.org 2023). Moreover, as a capital-scarce country, it required substantial investment in infrastructure. The economic situation in the country was exacerbated by the dire social conditions caused by war and the subsequent occupation of its territory by Armenia which led to a catastrophic rise in number of refugees and internally displaced persons (IDPs). Additionally, as a post-Soviet state, there was a widespread expectation among the population, which was accustomed to the Soviet welfare state model, that the state would take a leading role in alleviating these socio-economic issues (Luong and Weinthal 2010, 246). Thus, it is not surprising that oil revenues were spent heavily in the early 2000s, and the “Long-Term Strategy” mentioned above also envisioned using oil revenues to develop non-oil sectors.

Analysis of the economic effectiveness of this spending is beyond this article’s scope, although there are views that in general, it was not always prudent (e.g. Gurbanov et al. 2017). It is also evident that, by 2013, there was a noticeable trend toward overspending from the fund. Additionally, given that Azerbaijan’s peak oil production period was brief, and it was anticipated that production would face a structural decline by the decade’s end, the country had less time to indulge in capital investment. There was clearly an urgent need for a change in strategy to begin at least partial reduction of the budget transfers. This became evident in 2015 when the decline in global oil prices plunged Azerbaijan’s economy into crisis, exposing the vulnerabilities of its heavy reliance on the oil revenues. In response, the government, facing mounting pressure to stabilize the economy, initiated certain reforms aimed at reducing budget transfers from the fund (i.e. the budget rule), which were discussed earlier.

It would be difficult to argue that reforms enacted after 2015 were not largely triggered by the sharp decline in oil prices. But it is also important to consider the role of transparency in influencing the adoption changes specifically related to the fund. As SOFAZ’s assets had become a widely reported indicator of economic stability, the government did face a certain pressure to protect them. Additionally, considering SOFAZ’s important role as a symbol of economic stability, ensuring the sustainable growth of fund’s assets may have also been important for reinforcing the government’s credibility as well. Below these dynamics will be explored further.

4.2 Role of transparency: incentives and limitations

As discussed earlier, transparency is often regarded as a crucial mechanism for ensuring good governance in NRFs. However, its effectiveness also depends on the broader institutional context of the country. In institutionally strong societies, such as Norway, transparency adds to the existing oversight mechanisms over government spending. But in institutionally developing societies it is expected to compensate for the weakness of other oversight mechanisms. This means that, in developing societies with weaker institutional oversight, such as Azerbaijan, the impact of transparency is less unequivocal.

SOFAZ is frequently recognized for its transparency. For example, the Truman Scoreboard Index ranked it sixth among all evaluated funds, which makes it the top fund outside the OECD (Maire et al. 2021). Additionally, SOFAZ is a member of the International Forum of Sovereign Wealth Funds (IFSWF) and adheres to the Santiago Principles. Key details about the fund’s investment portfolio and transactions, including its full annual reports, both in Azerbaijani and English languages, are publicly accessible on its website. This means that financial information is available to any citizen of Azerbaijan or anyone from around the world. Moreover, SOFAZ’s financial statements are audited by reputable international firms, with PricewaterhouseCoopers handling the 2023 audit (SOFAZ Annual Report 2023, 9). Overall, there is a widespread agreement that, as far as collection and accumulation of revenue from the FOCs is concerned, SOFAZ is very transparent (Luong and Weinthal 2010). The roots of fund’s transparency can also be linked to its structure. It is isolated from rest of the government bureaucracy and primarily employs technocrats who have been educated overseas (Guliyev 2013). This allows SOFAZ to keep its internal transparency intact.

However, it should again be made clear that in this context, transparency specifically refers to the availability of public information about SOFAZ’s finances – that is, to the informational role of the NRFs mentioned earlier. Such transparency does not necessarily create actual legal constraints on the government’s ability to make withdrawals from the fund. However, it is also not purely symbolic, as it has played some role in shaping the policies regarding the fund.

The role of transparency in shaping SOFAZ’s fiscal policies becomes particularly evident after 2015. While the sharp decline in oil prices created immediate economic pressures, transparency mechanisms increased the political costs of solving these pressures through fund depletion. First, the fund (and notably its transparency) was usually mentioned and praised even before 2015 in speeches by officials (President.az 2011, President.az 2013). Over the years, regular public disclosures of SOFAZ’s financial figures meant that any reduction in assets would have to be reported. Such a reduction could be problematic for the government especially, since the local media typically covers these updates positively, highlighting the growth of assets as a notable achievement (Apa.az 2024a, Oxu.az 2024a). In fact, SOFAZ’s growth and sustainability of its assets have become a key indicator of the government’s effective management of oil revenues and is as such mentioned by the press editorials (Apa.az 2024b), government officials (Oxu.az 2024b), and even the president himself who has specifically emphasized the importance of growing the fund’s assets even during the crisis years, linking SOFAZ’s stability to broader economic credibility (President.az 2019).10

Therefore, a potential continuous decline in the fund’s assets would indicate a failure in managing oil revenues. Moreover, there is also relatively open discussion in the media about the importance of safeguarding the fund’s assets and the risks of relying too heavily on budget transfers (Mammadov 2023). Even the government’s flagship initiative “Azerbaijan 2030: National Priorities for Socio-Economic Development” explicitly mentions the need to lower the share of budget transfers (President.az 2021). It is difficult to imagine the government depleting the fund in such an environment. Thus in Azerbaijan, unlike other developing resource-exporting states where NRF depletion occurred with little or no public awareness (e.g. Venezuela), public availability of information regarding fund finances makes depletion politically costly. Particularly given that SOFAZ’s success and growth have been closely linked to political legitimacy at the highest level (President.az 2019).11

All of the above suggests that in the case of SOFAZ, transparency functions as an important informational tool that provides certain incentives for the government to protect the sustainability of the fund. Without public disclosure of information on the fund’s finances, this outcome would likely not have been achieved. However, it should also be stressed that this transparency is selective. It applies, for the most part, to the oil revenues coming into the fund, while expenditures once transferred to the state budget are less transparent. The government also retains considerable control over the fund’s budget transfers, and oversight mechanisms are still limited, especially considering the absence of independent members in the supervisory board. Therefore, while transparency has undoubtedly contributed to the sustainability of the fund, it should not be mistaken for true accountability

In broader terms, the case of SOFAZ indicates that the role of transparency within NRFs in developing countries is complex. One on hand, availability of public information has contributed to the sustainability of SOFAZ. In contrast, the Kazakhstani NFRK, is less transparent in terms of the availability of public information. Its annual reports are not made public in full (Kalyuzhnova 2011), and its relatively opaque nature – being managed by the National Bank rather than operating as an independent entity – means that it is not rated on the Truman Scoreboard Index. This lack of transparency could have contributed to the fluctuating size of the fund, as assets between 2014 and 2023 fell by 15 billion US dollars.

However, the SOFAZ case also shows that transparency alone is not a straightforward solution to challenges faced by NRFs due to weak oversight. While transparency has supported SOFAZ’s sustainability, it has not been effective in addressing other related issues. For example, an analysis of the Dutch disease effects in Azerbaijan would likely suggest the country suffers from it, pointing to the fund’s limited effectiveness in this area. Therefore, while having an NRF with transparency is beneficial, other factors like oversight are also critical for ensuring broader fund effectiveness.

There are concerns that NRFs in developing societies may struggle to effectively stabilize budget or save resource revenues due to weak oversight and various spending pressures, both objective and self-serving. Although it would be inaccurate to claim that Azerbaijan’s NRF completely disproves these concerns, it does demonstrate that, under certain circumstances, NRFs can help save resource revenues in developing societies. Clearly, the establishment of an NRF in Azerbaijan – particularly at such an early stage of oil production – was a crucial choice. Without this fund, the country would almost certainly be facing the post-oil period without any savings. Although SOFAZ has its limitations, it has managed to accumulate substantial assets for a nation of Azerbaijan’s size.

However, it is widely recognized that Azerbaijan has passed the peak of its oil revenues and faces a structural decline in terms of its oil production (IMF 2024). While the exploitation of the remaining reserves will continue and there are signed and operational agreements with the FOCs, it is anticipated that revenues from these will decrease. Azerbaijan does have gas reserves, and gas production is increasing but these will only partially compensate for the losses from the decreasing oil production (IMF 2024). While post-2015 reforms have introduced some budgetary discipline, the ability to sustain these measures in an environment where oil revenues will decline remains uncertain.

As oil revenues decline, the government may rely more heavily on SOFAZ to finance budget deficits. Without strict enforcement of fiscal rules, this could lead to depletion of fund assets over time. SOFAZ’s transparency mechanisms – regular financial reports, independent audits, and public disclosures – have helped create political incentives for the government to protect the fund assets. Whether this still continues to be the case in a post-oil era remains to be seen, especially given some concerning signs on the matter. For example, Azerbaijan was one of the first three Extractive Industries Transparency Initiative (EITI) pilot cases in 2002 and was designated as an EITI-compliant country in 2009 (Frynas 2017). However, in 2017 the country decided to withdraw from the EITI (Eiti.org 2017). While so far this has not affected the availability of public information regarding the fund, if revenues were to fall significantly as reserves decline, the government may seek greater flexibility in fund withdrawals. In such a case, the existing transparency mechanisms may be curbed.

While transparency is one factor in SOFAZ’s sustainability, the effectiveness of fiscal policies is also important. In this context, the newly adopted budget rule is a positive development. But it has been criticised for not setting a strict limit on the amount of an annual transfer from SOFAZ (Aghayev 2021). Moreover, the rule is not directly linked to the size of the fund’s assets but rather to the non-oil deficit. The guidelines allowing the government to suspend or alter the budget rule are also relatively soft (Aghayev 2021). While theoretically, this may be beneficial, in emergencies like pandemics that require urgent transfers, it is important to reduce this flexibility as oil revenues decline. In practice, this means adhering to the October 2023 decree discussed above and gradually lowering the ratio of the non-oil base deficit to the non-oil GDP. At a minimum, it is crucial to keep the share of budget transfers at its current level of one-third of budget revenues and not to increase it.

Perhaps the most economically viable way of protecting the fund’s assets is to expand the non-oil related budget revenues. In recent years, the non-oil related taxation revenue (excluding the taxes paid by the FOCs) has been growing. By the end of 2023 it accounted for 27.6 percent of the budget revenues, up from 22.1 percent in 2018 (Maliyye.gov.az 2023, 7). This rise is promising. The government has also adopted a strategy for socio-economic growth for the period of 2022-2026 (President.az 2022) in another attempt to boost the non-oil sector which currently contributes, a very small share to the country’s exports. The effectiveness of this is currently difficult to predict.

In terms of SOFAZ itself there are also possibilities of increasing the income through sources other than oil revenues. There are signs indicating that the fund may gradually shift away from its conservative investment approach. For instance, in 2019, equities made up 14.1 percent of the SOFAZ investment portfolio (SOFAZ Annual Report 2023). By 2023, this share had risen to 24.3 percent, approaching the upper threshold of 25 percent set by the fund’s Investment Guidelines (SOFAZ Annual Report 2023). It remains to be seen whether this threshold will be increased. The gradual increase in equity holdings might be an effort to boost investment returns in response to declining oil revenues. However, it is unlikely that the fund will fully abandon its conservative investment policy, as the risks of potential losses from equity investments would be too great.

Finally, Azerbaijan’s ability to sustain SOFAZ in the post-oil era will depend not just on economic policies, but on the strength of its institutional and transparency mechanisms. If transparency remains intact, political incentives may discourage excessive withdrawals, ensuring fund sustainability. If transparency weakens, economic pressures could lead to increased SOFAZ withdrawals, as has been the case in other developing societies. However, reforms – such as stricter fiscal rules and greater oversight – will also be necessary to ensure long-term fiscal discipline. Therefore, as oil revenues decline over the next decade, choices made by the government will decide if SOFAZ can successfully transition into a sustainable, long-term NRF or whether it will face depletion.

Ackah, Ishmael, and Denis M Gyeyir. 2021. “Saving Today’s Bread for Tomorrow’s Consumption? The Politics of Trade-Offs in the Governance of Ghana’s Petroleum Funds”. In Eyene Okpanachi and Reeta Chowdhari Tremblay (eds) The Political Economy of Natural Resource Funds International Political Economy Series, 117-145. Chem: Palgrave Macmillan. https://doi.org/https://doi.org/10.1007/978-3-030-78251-1_6.

Aghayev, Rovhsan. 2021. “Two New Budget Rules in Three Years. What Changed and Why?” Baku Research Institute. 27 December 2021. https://bakuresearchinstitute.org/en/two-new-budget-rules-in-three-years-what-changed-and-why-2/.

Altstadt, Audrey. 2017. Frustrated Democracy in Post-Soviet Azerbaijan. Frustrated Democracy in Post-Soviet Azerbaijan. New York City: Columbia University Press. https://doi.org/10.7312/alts70456.

Ambe-Uva, Terhemba N, and Sarah J Martin. 2021. “The Entanglements of Natural Resource Funds: Fundo Soberano de Angola and Domestic Political Interests”. In Eyene Okpanachi and Reeta Chowdhari Tremblay (eds) The Political Economy of Natural Resource Funds International Political Economy Series, 37-62. Chem: Palgrave Macmillan. https://doi.org/10.1007/978-3-030-78251-1_3.

Apa.Az. 2024a. “Dövlət Neft Fondunun aktivləri 58 mlrd. dolları ötüb”. Apa.az, 17 July 2024. https://apa.az/finance/dovlet-neft-fondunun-aktivleri-58-mlrd-dollari-otub-855342.

Apa.Az. 2024b. “ARDNF və Azərbaycan iqtisadiyyatı: 25 illik uğurlu yol”. Apa.az, 16 July 2024. https://apa.az/maliyye/ardnf-ve-azerbaycan-iqtisadiyyati-25-illik-ugurlu-yol-arasdirma-855212.

Auty, Richard. 1993. Sustaining Development in Mineral Economies. London: Routledge. https://doi.org/10.4324/9780203422595.

Bauer, Andrew. 2014. “Managing the Public Trust: How to Make Natural Resource Funds Work for Citizens”. https://www.resourcegovernance.org/sites/default/files/NRF_RWI_Complete_Report_EN.pdf.

Beblawi, Hazem. 1987. “The Rentier State in the Arab World”. Source: Arab Studies Quarterly. Vol. 9, no. 4: 383-398.

Bernstein, Shai, Josh Lerner, and Antoinette Schoar. 2013. “The Investment Strategies of Sovereign Wealth Funds”. Journal of Economic Perspectives 27, no. 2: 219–38. https://doi.org/10.1257/jep.27.2.219.

Bonaventura Altuve, Leonardo Di. 2024. “The Demise of Sovereign Wealth Funds”. Review of International Political Economy 31, no.1: 277-303. https://doi.org/10.1080/09692290.2023.2190601.

Collier, Paul, Rick Van Der Ploeg, Michael Spence, and Anthony J Venables. 2010. “Managing Resource Revenues in Developing Economies”. IMF Staff Papers 57 (1): 84–118. https://doi.org/10.1057/imfsp.2009.16.

Corden, W. M. 1984. “Booming Sector and Dutch Disease Economics: Survey and Consolidation”. Oxford Economic Papers 36, no. 3: 359-380. https://doi.org/10.1093/oxfordjournals.oep.a041643.

Corden, W. Max, and J. Peter Neary. 1982. ‘Booming Sector and De-Industrialisation in a Small Open Economy’. The Economic Journal 92 no. 368: 825-848. https://doi.org/10.2307/2232670.

Data.Worldbank.Org. 2023. “GDP (current US$) – Azerbaijan”. World Bank. https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=AZ.

Davis, Jeffrey M., Rolando Ossowski, James A. Daniel, and Steven Barnett. 2003. “Stabilization and Savings Funds for Nonrenewable Resources: Experience and Fiscal Policy Implications”. In Jeffrey Davis, Rolando Ossowski and Annalisa Fedelino (eds) Fiscal Policy Formulation and Implementation in Oil-Producing Countries, 273-316. Washington D.C.: INTERNATIONAL MONETARY FUND. https://doi.org/10.5089/9781589061750.071.

Deléchat, Corinne, Mauricio Villafuerte, and Shu-Chun S. Yang. 2017. “‘Best-Practice’ Sovereign Wealth Funds for Sound Fiscal Management”. In Malan Rietveld and Perrine Toledano (eds) The New Frontiers of Sovereign Investment, 11–25. New York City: Columbia University Press. https://doi.org/10.7312/riet17750-004.

Eiti.Org. 2017. “Azerbaijan withdraws from the EITI”. EITI, 10 March 2017. https://eiti.org/news/azerbaijan-withdraws-eiti.

E-Qanun.Az. 2023. “AZƏRBAYCAN RESPUBLİKASI PREZİDENTİNİN FƏRMANI”. E-Qanun.az, 24 October 2023. https://e-qanun.az/framework/55431.

Erdmann, Gero, and Ulf Engel. 2006. “Neopatrimonialism Revisited: Beyond a Catch-All Concept”. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.909183.

Fisun, Oleksandr. 2019. “Neopatrimonialism in Post-Soviet Eurasia”. In Balint Magyar (editor) Stubborn Structures, 75–96. Central European University Press. https://doi.org/10.1515/9789633862155-006.

Franke, Anja, Andrea Gawrich, and Gurban Alakbarov. 2009. “Kazakhstan and Azerbaijan as Post-Soviet Rentier States: Resource Incomes and Autocracy as a Double ‘curse’ in Post-Soviet Regimes”. Europe - Asia Studies 61 no. 1: 109–140. https://doi.org/10.1080/09668130802532977.

Frynas, Jedrzej George. 2017. “Sovereign Wealth Funds and the Resource Curse: Resource Funds and Governance in Resource-Rich Countries”. In Douglas J Cumming, Geoffrey Wood, Igor Filatotchev, and Juliane Reinecke (eds) The Oxford Handbook of Sovereign Wealth Funds, 123-142. Oxford University Press.

Gel’man, Vladimir. 2016. “The Vicious Circle of Post-Soviet Neopatrimonialism in Russia”. Post-Soviet Affairs 32 no. 5: 455–73. https://doi.org/10.1080/1060586X.2015.1071014.

Guliyev, Farid. 2013. “Oil and Regime Stability in Azerbaijan”. Demokratizatsiya: The Journal of Post-Soviet Democratization 21 no. 1: 113–47.

Guliyev, Farid. 2020. “Formal-Informal Relations in Azerbaijan”. Caucasus Analytical Digest, no. 114 (March). https://doi.org/10.3929/ethz-b-000400500.

Gurbanov, Sarvar, Jeffrey Nugent, and Jeyhun Mikayilov. 2017. “Management of Oil Revenues: Has That of Azerbaijan Been Prudent?” Economies 5 no. 2: 19. https://doi.org/10.3390/economies5020019.

Humphreys, Macartan, and Martin E Sandbu. 2007. “The Political Economy of Natural Resource Funds”. Macartan Humphreys, Jeffrey D Sachs, and Stiglitz Joseph E. (eds) Escaping the Resource Curse, 194-233. New York City: Columbia University Press.

IMF. 2024. “IMF Executive Board Concludes 2023 Article IV Consultation with the Republic of Azerbaijan”. IMF. 2024. https://www.imf.org/en/News/Articles/2024/02/06/pr2441-azerbaijan-imf-executive-board-concludes-2023-article-iv-consultation.

Izquierdo-Brichs, Ferran, and Francesc Serra-Massansalvador, eds. 2021. Political Regimes and Neopatrimonialism in Central Asia. Singapore: Springer Singapore. https://doi.org/10.1007/978-981-15-9093-1.

Kalyuzhnova, Yelena. 2011. “The National Fund of the Republic of Kazakhstan (NFRK): From Accumulation to Stress-Test to Global Future”. Energy Policy 39 no. 10: 6650–57. https://doi.org/10.1016/j.enpol.2011.08.026.

Karl, Terry Lynn. 1997. The Paradox of Plenty. Berkley: University of California Press. https://doi.org/10.1525/9780520918696.

Kendall-Taylor, Andrea. 2012. “Purchasing Power: Oil, Elections and Regime Durability in Azerbaijan and Kazakhstan”. Europe-Asia Studies 64 no. 4: 737–760. https://doi.org/10.1080/09668136.2012.671567.

Luong, Pauline Jones, and Erika Weinthal. 2010. Oil Is Not a Curse: Ownership Structure and Institutions in Soviet Successor States.

Cambridge: Cambridge University Press. https://doi.org/10.1017/CBO9780511779435.

Mahdavy, Hossein. 1970. “The Patterns and Problems of Economic Development in Rentier States: The Case of Iran”. In M.A Cook (editor) Studies in the Economic History of the Middle East, 428–67. London: Oxford University Press.

Maire, Julien, Adnan Mazarei, and Edward M Truman. 2021. “Sovereign Wealth Funds Are Growing More Slowly, and Governance Issues Remain”. https://www.piie.com/sites/default/files/documents/pb21-3.pdf.

Maliyye.Gov.Az. 2023. “Azərbaycan Respublikasının 2023-cü il dövlət büdcəsinin icrasına dair illik HESABAT”. https://maliyye.gov.az/scripts/pdfjs/web/viewer.html?file=/uploads/static-pages/files/6682702853f54.pdf.

Mammadov, Elnur. 2023. “Ильхам Алиев констатирует… и снижаются трансферты в бюджет из Нефтяного фонда” Haqqin.az. 20 April 2023. https://haqqin.az/oldage/281173.

Markowitz, Chelsea. 2020. “Sovereign Wealth Funds in Africa: Taking Stock and Looking Forward”. https://saiia.org.za/wp-content/uploads/2020/02/Occasional-Paper-304-markowitz.pdf.

Mehlum, Halvor, Karl Moene, and Ragnar Torvik. 2006. “Institutions and the Resource Curse”. The Economic Journal 116, no. 508: 1–20. https://doi.org/10.1111/j.1468-0297.2006.01045.x.

Mien, Edouard, and Michaël Goujon. 2022. “40 Years of Dutch Disease Literature: Lessons for Developing Countries”. Comparative Economic Studies 64, no. 3: 351–83. https://doi.org/10.1057/s41294-021-00177-w.

Moses, Jonathon W. 2021. “A Less Than Sovereign Wealth Fund: Norway’s Government Pension Fund, Global”. In Eyene Okpanachi and Reeta Chowdhari Tremblay (eds) The Political Economy of Natural Resource Funds International Political Economy Series, 1-14. Chem: Palgrave Macmillan. https://doi.org/10.1007/978-3-030-78251-1_8.

Okpanachi, Eyene, and Reeta Chowdhari Tremblay. 2021. “Introduction: The Political Economy of Natural Resource Funds (NRFs)”. In Eyene Okpanachi and Reeta Chowdhari Tremblay (eds) The Political Economy of Natural Resource Funds International Political Economy Series, 181-206. Chem: Palgrave Macmillan. https://doi.org/10.1007/978-3-030-78251-1_1.

Oxu.Az. 2024a. “ARDNF-in aktivləri 58 milyard dollara çatıb” Oxu.az, 17 July 2024. https://oxu.az/iqtisadiyyat/ardnf-in-aktivleri-58-milyard-dollara-catib.

Oxu.Az. 2024b. “Prezidentin köməkçisi: “Ölkəyə müxtəlif sektorlardan 300 milyard dollardan çox investisiya daxil olub” Oxu.az, 2 May 2024. https://oxu.az/siyaset/prezidentin-komekcisi-olkeye-muxtelif-sektorlardan-300-milyard-dollardan-cox-investisiya-daxil-olub-video.

Ploeg, Frederick van der, and Anthony J. Venables. 2011. “Harnessing Windfall Revenues: Optimal Policies for Resource‐Rich Developing Economies”. The Economic Journal 121, no. 551: 1–30. https://doi.org/10.1111/j.1468-0297.2010.02411.x.

President.Az. 2011. “Ilham Aliyev attended the opening ceremony of the international festive event marking the 20th anniversary of the state independence of the Republic of Azerbaijan” President.az, 23 September 2011. https://president.az/en/articles/view/3158.

President.Az. 2013. “Ilham Aliyev attended the opening ceremony of the First South Caucasus Forum” President.az, 7 May 2013. https://president.az/en/articles/view/8018.

President.Az. 2016. “Milli iqtisadiyyat və iqtisadiyyatın əsas sektorları üzrə strateji yol xəritələrinin təsdiq edilməsi haqqında Azərbaycan Respublikası Prezidentinin Fərmanı” President.az, 6 December 2016. https://president.az/az/articles/view/21953.

President.Az. 2019. “Ilham Aliyev received Israfil Mammadov in connection with his appointment to new post” President.az, 29 November 2019. https://president.az/en/articles/view/35013.

President.Az. 2021. “Order of the President of the Republic of Azerbaijan on approval of “Azerbaijan 2030: National Priorities for Socio-Economic Development” President.az, 2 February 2021. https://president.az/en/articles/view/50474.

President.Az. 2022. “Azərbaycan Respublikasının 2022-2026-cı illərdə sosial-iqtisadi inkişaf Strategiyası” President.az, 22 July 2022, https://static.president.az/upload/Files/2022/07/22/5478ed13955fb35f0715325d7f76a8ea_3699216.pdf.

Prichard, Wilson, Paola Salardi, and Paul Segal. 2018. “Taxation, Non-Tax Revenue and Democracy: New Evidence Using New Cross-Country Data”. World Development 109 (September): 295–312. https://doi.org/10.1016/j.worlddev.2018.05.014.

Robinson, Neil. 2012. “Institutional Factors and Russian Political Parties: The Changing Needs of Regime Consolidation in a Neo-Patrimonial System”. East European Politics 28, no. 3: 298–309. https://doi.org/10.1080/21599165.2012.685629.

Ross, Michael L. 2012. The Oil Curse. Princeton University Press. https://doi.org/10.1515/9781400841929.

Roy, Bimal Chandra, Satyaki Sarkar, and Nikhil Ranjan Mandal. 2013. “Natural Resource Abundance and Economic Performance – A Literature Review”. Current Urban Studies 01 no. 04: 148–55. https://doi.org/10.4236/cus.2013.14016.

Sachs, Jeffrey, and Andrew Warner. 1995. “Natural Resource Abundance and Economic Growth”. Working Paper. Cambridge, MA. https://doi.org/10.3386/w5398.

Sanchez, Emerson M., and Jayson S. Lamchek. 2023. “Creating a Sovereign Wealth Fund in a Corruption-Riddled Country: Energizing Transparency and Sound Governance with Direct Benefit-Sharing”. Resources Policy 81: 1-11. https://doi.org/10.1016/j.resourpol.2022.103244.

Segura, Alonso. 2006. “Management of Oil Wealth Under the Permanent Income Hypothesis: The Case of São Tomé and Príncipe”. IMF Working Paper 06/183. https://www.imf.org/external/pubs/ft/wp/2006/wp06183.pdf.

Shkel, Stanislav N. 2019. “Neo-Patrimonial Practices and Sustainability of Authoritarian Regimes in Eurasia”. Communist and Post-Communist Studies 52 no. 2: 169–76. https://doi.org/10.1016/j.postcomstud.2019.04.002.

Snudden, Stephen. 2016. “Cyclical Fiscal Rules for Oil-Exporting Countries”. Economic Modelling 59 (December): 473–483. https://doi.org/10.1016/j.econmod.2016.08.009.

SOFAZ Annual Report. 2023. “Annual Report 2023” Baku. https://www.oilfund.az/en/report-and-statistics/get-download-file/flip/7_2023_tam_en.pdf.

‘SOFAZ Mission and Objectives’. 2025. “Mission and Objectives” oilfund.az, 2025. https://www.oilfund.az/en/fund/about/mission.

‘SOFAZ Recent Figures’. 2025. “Recent Figures” oilfund.az, 2025. https://www.oilfund.az/en/report-and-statistics/recent-figures.

Statista.com. 2025. “Average annual Brent crude oil price from 1976 to 2025” statista.com, https://www.statista.com/statistics/262860/uk-brent-crude-oil-price-changes-since-1976/.

Time.Kz. 2024. 11 June 2024. “На $1,7 млрд снизились валютные активы Нацфонда Казахстана в апреле – Нацбанк” time.kz, https://time.kz/news/economics/2024/06/11/na-1-7-mlrd-snizilis-valyutnye-aktivy-natsfonda-kazahstana-v-aprele-natsbank.

Umudov, Agshin. 2021. Asymmetric Environmental Governance in Azerbaijan. Cham: Springer International Publishing. https://doi.org/10.1007/978-3-030-82116-6.

Venables, Anthony J. 2016. “Using Natural Resources for Development: Why Has It Proven so Difficult?” Journal of Economic Perspectives 30, no. 1: 161-184 https://doi.org/10.1257/jep.30.1.161.

1 In literature and media, NRFs are also often referred to as Sovereign Wealth Funds (SWFs). SWFs are state-owned investment funds (comprised of bonds, stocks, properties etc.) that are funded by government surplus revenues. This surplus can emerge because of the excess natural resource revenues (which would make the SWF a commodity-based fund) or might arise due to some other reasons (e.g. fiscal surplus). In this article, to differentiate them from non-commodity-based SWFs, the term NRF will be used for commodity-based SWFs, a designation also adopted by other researchers (e.g. Humphreys and Sandbu 2007, Okpanachi and Tremblay 2021)

2 Founded in 1953, the Kuwait Investment Authority (KIA) is the oldest such fund in the world.

3 The practice in resource-rich countries of reducing public spending during periods of high revenues or economic booms. Its opposite is procyclical spending, where governments increase spending during boom periods.

4 The IFSWF was founded in 2008 as a voluntary association of sovereign wealth funds worldwide. Incidentally, its first meeting, held in 2009, was hosted by SOFAZ in Baku. Santiago Principles adopted by IFSWF consist of 24 voluntary principles (called Generally Accepted Principles and Practices – GAPP), relating to transparency, governance, and accountability.

5 The Truman Scoreboard Index developed by the Peterson Institute for International Economics (PIIE), uses 33 individually weighted indicators covering four key categories: structure, governance, transparency/accountability and behaviour.

6 Notably, post-Soviet states, including Azerbaijan, have been described as neopatrimonial in number of studies (Robinson 2012, Gel’man 2016, Fisun 2019, Shkel 2019, Izquierdo-Brichs and Serra-Massansalvador 2021). In the Weberian framework, patrimonialism is seen as a form of traditional authority, where a political and economic system is built on the use of public power for personal gain (Gel’man 2016). Neopatrimonialism extends this logic into modern societies. It is characterized by “informal institutional “core,” or de facto constitution, of the neopatrimonial politico-economic order, around which the ruling groups build the shell of formal institutions (such as official constitutions or electoral systems)” (Gel’man, 2016, 459). However, these formal institutions are functional rather than merely symbolic, even though informal practices significantly influence their operation (Erdmann and Engel 2006, Shkel 2019). Other features of neopatrimonialism include personalism, rent-seeking, corruption, and prebendalism (Shkel 2019).

7 Since the document was repealed, it is no longer available on the SOFAZ website but can still be accessed through: https://web.archive.org/web/20161213073848/https://www.oilfund.az/uploads/5-eng-long-term.pdf.

8 The deficit of the national budget once the revenues from oil and gas exports are excluded. Setting a limit on non-oil deficit restricts the extent to which oil revenues can be used to finance the non-oil deficit, ensuring it does not exceed a specified threshold.

9 For more in-depth explanation of the rule see Aghayev (2021).

10 See the following quote from the speech given by President during the meeting with the new SOFAZ CEO: “The main thing is that over the 20 years we have not lost funds and have increased the Fund’s resources every year. Even in the crisis years, when we were faced with devaluation, the Fund’s savings did not decrease. I did not allow that to happen. We reduced costs, resorted to major saving measures, maintained our strategic foreign exchange reserves and increased them. I can say that this happens very rarely, because at a time when oil prices fell sharply, fourfold, all sovereign funds lost a lot of money. They lost billions, tens of billions of dollars, but we did not lose anything because we are pursuing a very thoughtful policy.” (Para. 6).

11 See the following quote from the speech given by President during the meeting with the new SOFAZ CEO: “I must also say that the proposal to establish the Oil Fund was submitted to the great leader by me. At that time, there were different opinions in the government, and some members of the government opposed the idea. Their suggestion was that all oil revenues should go into the state budget and be spent annually. If that approach had been chosen, there would be no money in our State Oil Fund today. I opposed the idea, tried to prove that in order to store the funds in a transparent manner, channel them into strategic areas of our country and save them for future generations, there must be a State Oil Fund, and I achieved this” (Para. 4).